A simpler, more powerful retirement plan

for Connecticut employers

Not all Connecticut employers are required to register for MyCTSavings, but those who meet the criteria must either join the program or offer their own qualified plan. A WealthRabbit SIMPLE IRA gives employers more flexibility and control, valuable tax advantages, and easy payroll integration, making it a modern, compliant, and employee-friendly alternative.

What is MyCTSavings?

MyCTSavings is Connecticut’s state-mandated retirement savings program for employers that do not offer a private retirement plan. The state mandate includes employers with five or more employees who have been paid for at least the last 12 months. Employees become eligible once they are at least 19 years old and have been employed for a minimum of 120 days, with a default contribution rate of 5% of gross pay.

Registration deadlines

The registration deadline depends on the size of your business:

- Businesses with 100+ employees: June 30, 2022

- Businesses with 26 to 99 employees: October 31, 2022

- Businesses with 5 to 25 employees: March 30, 2023

- Newly eligible businesses: August 31 of each year

Non-compliance penalties

If noncompliance continues for 90 days or more, annual fines are imposed based on the number of employees:

- Up to $500 per year (5–24 employees)

- Up to $1,000 per year (25–99 employees)

- Up to $1,500 per year (100+ employees)

What you’re missing with MyCTSavings

MyCTSavings is designed to check a compliance box - but for businesses and employers, it often falls short:

- Limited investment optionsEmployees can't build customized retirement portfolios.

- No employer benefitsBusinesses spend time managing compliance, but don't receive tax incentives.

- One-size-fits-allEvery business is forced into the same model, regardless of size or needs.

- Minimal growth potentialLimited funds can mean lower returns for employees over time.

- Harsh penaltiesNon-compliant businesses may face annual fines of up to $1,500

Ready for a retirement solution that works better for your business?

SIMPLE IRA: The smart alternative to MyCTSavings

A SIMPLE IRA plan offers significant advantages over the state-mandated option, providing tax benefits for employers and greater growth potential for employees. It's a powerful tool for attracting and retaining talent.

- Tax credits Qualify for up to $5,500 in tax credits for starting a new plan.

- Employer tax deductions Contributions you make are tax-deductible as a business expense.

- Higher contribution limits Both employees and employers can contribute significantly more than with MyCTSavings.

- Investment flexibilityEmployees get access to a wide range of investment options, not just a few target-date funds.

- Attract & retain talentOffering a superior retirement benefit makes your company more competitive.

See How Much You Can Save with a SIMPLE IRA

Small businesses can take advantage of tax credits to help cover setup and administrative costs. By launching a new plan with auto-enrollment, you could qualify for up to $5,500 in tax credits!

How tax credits work

Tax credits are designed to offset the cost of setting up and administering, as well as contributing to the employees retirement savings.

Employers can claim up to $5,000 per year for three years to offset plan setup and administrative costs. They may qualify for additional tax credits.

- Auto-enrollment bonusIf you make the plan automatic (employees are enrolled unless they opt out), you get an extra $500 credit for 3 years.

- Employer contributionsYou may also get credits for money you put into employees' accounts (up to $1,000 per employee in the early years).

Together, these credits can add up to thousands in savings for your business. Curious how much you could claim?

Try our calculator and see exactly how much you could save.

Estimate your tax credit

Disclosure*

The SIMPLE IRA tax credit calculator is intended to estimate the average tax credit for your business. Please note, it does not constitute tax or legal advice.

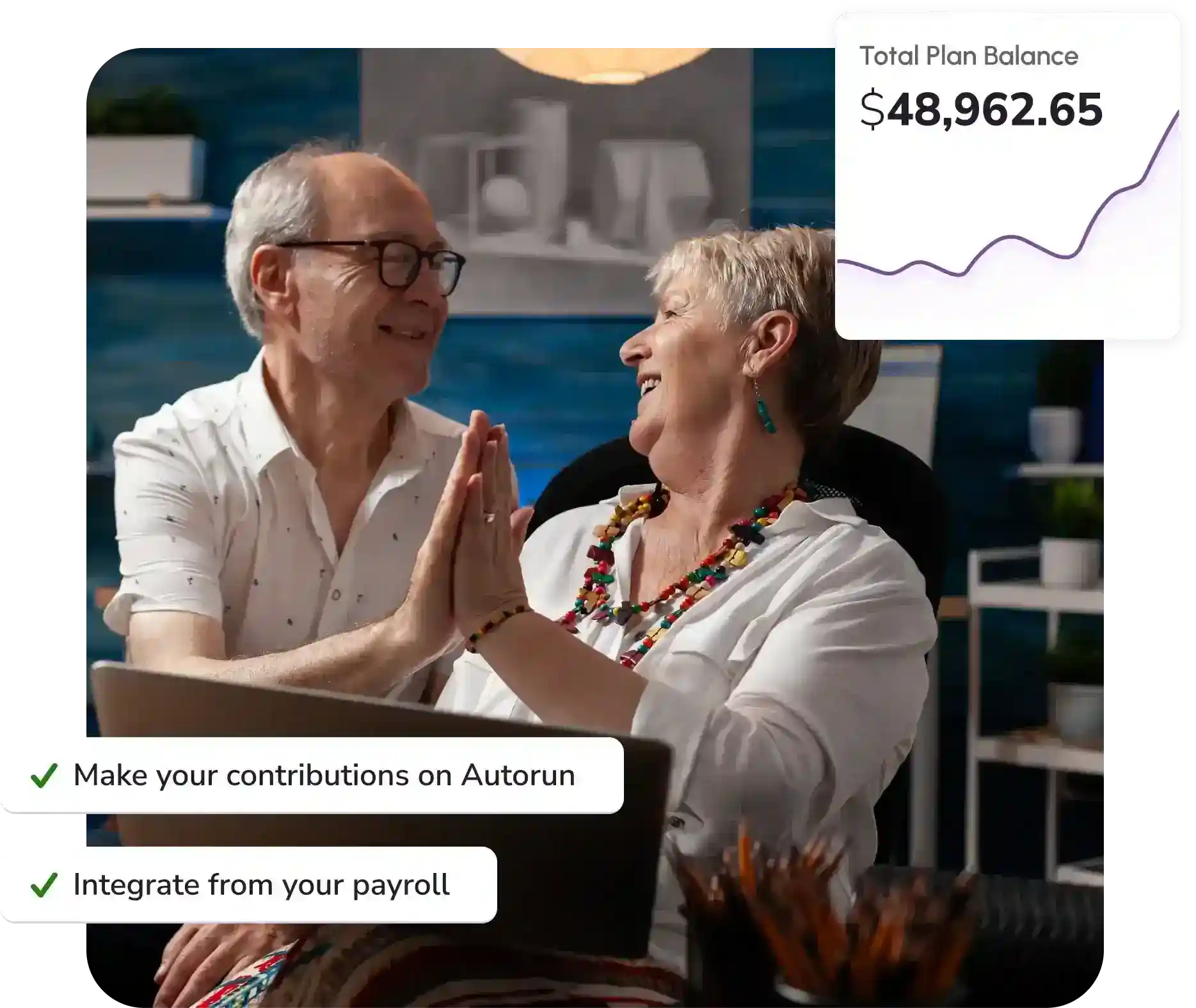

Elevate your retirement savings with WealthRabbit

Instead of enrolling in MyCTSavings, Connecticut businesses can choose a WealthRabbit SIMPLE IRA — a smarter way to stay compliant while giving employees more value.

- Self-onboardingEmployers and employees sign up on their own—retirement plans are up and running in just a few clicks.

- Seamless payroll integrationWealthRabbit seamlessly connects with your payroll system to ensure accurate and timely contributions for every employee.

- Streamlined plan rolloversEasily roll funds from your existing retirement plan into WealthRabbit— no hassle, no delays.

- Automated contributionsEnjoy a hands-off approach to retirement savings. Set up automatic deposits so your team never misses a contribution.

- Employee & employer portalsManage contributions and investments anytime, anywhere — with real-time access to performance and account activity.

MyCTSavings vs. WealthRabbit

A quick look at how WealthRabbit’s SIMPLE IRA compares to Connecticut’s state program.

| Feature | MyCTSavings | WealthRabbit SIMPLE IRA |

|---|---|---|

| Administrative efforts | State-mandated with limited customization; minimal employer involvement | Streamlined process with automated setup and payroll integration |

| Retirement options | Roth IRA only; default 5% contribution and no employer match | More diverse investment options, customizable based on business needs |

| Eligibility criteria | Employers must have 5 or more employees, employees eligible if ≥19 years old and employed 120 days | Participation is open to employers with ≤100 employees earning ≥$5,000. A required contribution is either a 3% dollar-for-dollar match or a 2% nonelective contribution |

| Flexibility | State-regulated with fixed contribution rates and minimal flexibility | Highly customizable plan with the ability to modify contribution rated and match options |

| Monthly fees | No employer fees; participants pay about 0.23% in asset-based fees and a $26 annual account fee | User-friendly portals + mobile access + stronger growth Low-cost setup: $29/month + $4 per employee, no state fees |

| Employee experience | Basic account with limited tools for employees | Comprehensive dashboard, financial literacy resources, and rollover support |

Frequently asked questions

Private-sector employers in Connecticut must register for MyCTSavings or certify an exemption if they meet all of the following criteria:

- They have five or more employees in Connecticut

- They have paid those employees for at least the last 12 months.

- They have not offered a qualified retirement plan in the preceding 2 years

Eligible employees must be at least 19 years old and have been employed for at least 120 days. Employers who already offer a qualified plan (such as a SIMPLE IRA) must still certify their exemption through the MyCTSavings portal.

The MyCTSavings program launched in 2022, with phased registration deadlines that have already passed for most employers:

- 100+ employees: June 30, 2022

- 26 to 99 employees: October 31, 2022

- 5 to 25 employees: March 30, 2023

- Newly eligible businesses: August 31 of each year

For employers who become newly eligible, you must register or certify an exemption by August 31 of the year following notification from the state.

If you have questions about your specific deadline, contact WealthRabbit support for assistance.

TEmployers must facilitate the MyCTSavings program, but are not responsible for enrollment, investments, or distribution management. Their key obligations include:

- Registering or certifying an exemption via the MyCTSavings portal

- Supplying employer, payroll, banking, and employee roster data

- Providing eligible employees (age 19+, worked 120 days) with program notices and documentation

- Deducting employee contributions via payroll and remitting them on schedule

- Maintaining records: updating employee status, handling rate changes, adding new hires, marking terminations

Employers are prohibited from making matching or employer contributions to MyCTSavings accounts.

Employers that fail to register or certify an exemption may face annual fines after 90 days of noncompliance:

- 5-24 employees: Up to $500 per year

- 25-99 employees: Up to $1,000 per year

- 100+ employees: Up to $1,500 per year

Choosing a WealthRabbit SIMPLE IRA ensures your organization stays compliant while giving employees a more modern and flexible retirement benefit.

Retirement planning that supports your success

Join hundreds of small businesses and individuals building real financial security with

WealthRabbit - fully digital, fully automated, fully yours.